What is Medical Insurance?

Medical Insurance is a financial safety net that protects you from the rising cost of medical treatment. With increasing healthcare expenses in India, having a health plan has become essential for both individuals and families. It ensures that you receive timely, quality medical care without stressing about hospital bills.

A medical insurance policy typically covers expenses like hospitalization, surgeries, daycare procedures, critical illness treatments, and more depending on the plan. Many people prefer medical insurance plans that offer wide coverage, cashless treatment facilities, and affordable premiums.

Choosing the right plan helps you stay financially prepared for unexpected medical emergencies. Whether you need an individual plan, family floater plan, senior citizen plan, or a comprehensive policy, It plays a vital role in securing your health and future.

Benefits of Medical Insurance

Medical insurance offers several important benefits that protect you during medical emergencies. One of the biggest advantages is that it saves you from paying large hospital bills, as the insurer handles most of the expenses depending on your sum.

Enjoy cashless treatment, surgery coverage, room rent support, and protection for pre and post-hospitalization expenses. Many plans also include annual health check-ups and coverage for advanced medical treatments.

Another key benefit is financial security. Whether it’s an individual plan or a family floater plan, Insurance ensures that a sudden illness or accident does not disturb your savings.

Types of Medical Insurance

Understanding the types of medical insurance helps you choose the right plan according to your needs:

a) Individual Medical Insurance - Covers only one person with personalized benefits.

b) Family Floater Medical Insurance - A single sum insured is shared among the entire family and often includes attractive discounts.

c) Senior Citizen Medical Insurance - Designed for people above 60 years, covering age-related illnesses.

d) Critical Illness Medical Insurance - Offers a lump-sum payout upon diagnosis of major illnesses like cancer or heart disease.

e) Group Medical Insurance - Provided by employers for employees with basic coverage at low premiums.

f) Top-up & Super Top-up Plans - Increase your coverage at an affordable cost.

Each plan serves a different purpose, and the right choice depends on age, family size, medical history, and budget.

Eligibility Criteria for Medical Insurance

Before purchasing a medical insurance plan, it is important to understand the basic eligibility criteria:

a) Minimum & Maximum Entry Age – Minimum entry age is usually 18 years, and maximum entry age ranges from 65 years to lifelong renewability. Children can be covered from 90 days to 30 years depending on the plan.

b) Pre-Policy Medical Test – Some people may need medical tests, especially senior citizens or those with existing medical issues.

c) Sum Insured Options – Your sum insured depends on needs and family size. In today's time, a minimum of ₹10 lakh is recommended.

Meeting these criteria ensures smooth issuance of your policy.

What Factors Affect Medical Insurance Premium?

Several factors impact the medical insurance premium, and understanding them helps you choose the right plan:

a) Age - Younger people pay lower premiums. Premiums increase with age, especially after 60.

b) Past Medical History - Existing diseases or past medical records can increase the premium.

c) Life style Habits - Smoking, alcohol consumption, or other unhealthy habits raise medical risks, increasing your premium.

d) Optional Covers - Riders such as critical illness cover, accident cover, hospital cash, room-rent waiver etc. increase the premium.

Medical Insurance Tax Benefit

One major advantage of buying medical insurance is the tax benefit available under Section 80D of the Income Tax Act. You can claim tax deductions on the premium you pay for yourself, spouse, children, and parents. Individuals under 60 years of age are eligible for a tax deduction of up to ₹25,000, while senior citizens are eligible for a higher deduction of up to Rs. 50,000.

This benefit not only reduces taxable income but also encourages better financial planning.

Medical Insurance Plans

There are many medical insurance plans available in India for different medical and financial needs. Choosing the right plan depends on age, family size, lifestyle, and required coverage. Most insurers offer a wide range of plans from basic hospitalization cover to comprehensive policies with maternity benefits, critical illness cover, OPD care, and more. When looking for the best insurance in India, you should consider:

a) High claim settlement ratio

b) Wide hospital network

c) Affordable premium

d) Flexible sum insured

e) Good customer service

Comparing different medical insurance plans helps you get maximum value for money.

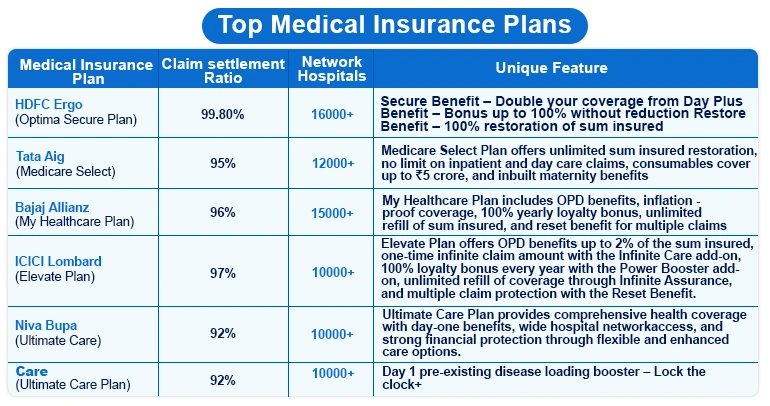

Top Medical Insurance Plans

What does Medical Insurance Basic Features Include?

A medical insurance plan generally includes:

a) In-Patient Hospitalization - Covers hospitalization expenses for more than 24 hours.

b) Pre & Post Hospitalization - Covers the medical costs you face before getting admitted and the expenses that continue after you’re discharged.

c) Daycare Procedures - Covers treatments like cataract, sinus treatment, and minor surgeries.

d) Ambulance Expenses - Covers road or air ambulance costs.

e) Domiciliary Treatment - Covers treatments at home when hospital admission isn’t possible.

f) Organ Donor Expenses - Covers organ donor hospitalization and surgery costs.

g) AYUSH Treatments - Covers Ayurveda, Homeopathy, Unani, Siddha, Yoga, and Naturopathy.

h) Annual Health Check-ups - Helps in early detection of health issues.

Exclusions in Medical Insurance

Medical insurance commonly exclude as follows:

a) Cosmetic surgeries unless medically necessary.

b) Routine dental, vision, or hearing treatment.

c) Lifestyle related diseases caused by smoking or substance abuse.

d) Self-inflicted injuries or suicide attempts.

e) Pregnancy related expenses unless covered under maternity benefit.

f) Diagnostic tests without diagnosis or hospitalization.

g) Drink and Drive.

How to File a Medical Insurance Claim?

1. Cashless claim process - When you are about to take your cashless claim then you have to submit below given documents.

a) Visit a network hospital

b) Show your policy card or number

c) Fill pre-authorization form

d) Hospital sends it to insurer

e) Once approved, treatment begins

f) Insurer settles the bill directly

2. Reimbursement claim process - In this process if you went to non-network hospital then you have to pay expenses from your side and then you have to submit the documents to your insurer. Documents list is as follows:

a) Pay the hospital bill at the time of discharge.

b) Collect the all original documents like bills, doctor consultation, payment receipts.

c) Fill the duly filled claim form and signed it.

d) Insurer verifies the documents.

e) Submit your kyc documents and cancel cheque.

f) After completed all documents, within 3 to 4 days you will received the claim amount in your bank.

Waiting Period in Medical Insurance

Waiting period in medical insurance refers to the time during which certain benefits of your insurance policy are not active. You can only claim for specific treatments or conditions once this time has passed. Every policy has different waiting timelines depending on the coverage. Here are some types:

1. Initial Waiting Period - The initial waiting period is the time during which you cannot raise a claim for any illness after buying your medical insurance policy. For the first 30 days, only accidental hospitalization is covered. Any seasonable disease like fever, dengue, malaria, etc. claim is accepted only after this period is completed.

2. Specific Waiting Period - The specific disease waiting period applies to specific disease such as hernia, piles, cataract, joint replacement, and similar conditions. These illnesses are covered only after completing the waiting period, which usually ranges from 1 to 2 years, depending on the medical insurance plans.

3. Pre Existing Disease Waiting Period - A pre-existing disease waiting period applies to any medical condition you already had before buying the policy, such as diabetes, hypertension, thyroid issues, asthma, etc. These conditions are covered only after completing 2 to 4 years of continuous policy coverage.

4. Maternity Waiting Period – The maternity waiting period applies if your medical insurance policy includes maternity benefits. Expenses related to pregnancy, delivery, and newborn care are covered only after completing the waiting period, which may vary from 9 months to 4 years, depending on the plan that you have opt.

Documents Required for Claim

When you file a claim under your medical insurance plans, the insurer verifies your treatment details and hospital records to process the request. Medical insurance policy ensures that you receive cashless or reimbursement claims without any kind of delays, by provided all required details correctly. Whether it’s a planned treatment or an emergency, proper documentation helps in faster claim settlement. In this insurance you can claim in types like in cashless insurance or reimbursement claim so in future if you need to take any claim here are the documents list that you need.

1. Cashless Claim - For opting cashless claim you have to arrange following documents:

a) Policy Copy

b) Valid ID proof (Aadhar and Pan)

c) Doctor Advice

d) Pre-authorization form (Rest process will do by hospital TPA)

2. Reimbursement - For reimbursement claim you have to arrange these following documents:

a) Original bills

b) Payment receipts

c) Discharge summary

d) Consultation papers

e) Medicine bills

f) Diagnostic reports

g) Filled claim form

e) Cancelled Cheque

5.0

Need advice from experts?

Don't guess your health cover, get expert guidance in one quick call.

Benefits of Medical Insurance

Medical insurance offers several important benefits that protect you during medical emergencies. One of the biggest advantages is that it saves you from paying large hospital bills, as the insurer handles most of the expenses depending on your sum.

Major benefits include cashless treatments, surgery coverage, room rent, pre & post-hospitalization expenses, and in many plans, annual health check-ups and modern treatment coverage.

Another key benefit is financial security. Whether it’s an individual plan or a family floater plan, Insurance ensures that a sudden illness or accident does not disturb your savings.

Types of Medical Insurance

Understanding the types of medical insurance helps you choose the right plan according to your needs:

a) Individual Medical Insurance - Covers only one person with personalized benefits.

b) Family Floater Medical Insurance - A single sum insured is shared among the entire family and often includes attractive discounts.

c) Senior Citizen Medical Insurance - Designed for people above 60 years, covering age-related illnesses.

d) Critical Illness Medical Insurance - Offers a lump-sum payout upon diagnosis of major illnesses like cancer or heart disease.

e) Group Medical Insurance - Provided by employers for employees with basic coverage at low premiums.

f) Top-up & Super Top-up Medical Plans - Increase your coverage at an affordable cost.

Each plan serves a different purpose, and the right choice depends on age, family size, medical history, and budget.

Eligibility Criteria for Medical Insurance

Before purchasing a medical insurance plan, it is important to understand the basic eligibility criteria:

a) Minimum & Maximum Entry Age – Minimum entry age is usually 18 years, and maximum entry age ranges from 65 years to lifelong renewability. Children can be covered from 90 days to 30 years depending on the plan.

b) Pre-Policy Medical Test – Some people may need medical tests, especially senior citizens or those with existing medical issues.

c) Sum Insured Options – Your sum insured depends on needs and family size. In today's time, a minimum of ₹10 lakh is recommended.

Meeting these criteria ensures smooth issuance of your policy.

What Factors Affect Medical Insurance Premium?

Several factors impact the medical insurance premium, and understanding them helps you choose the right plan:

a) Age - Younger people pay lower premiums. Premiums increase with age, especially after 60.

b) Past Medical History - Existing diseases or past medical records can increase the premium.

c) Life style Habits - Smoking, alcohol consumption, or other unhealthy habits raise medical risks, increasing your premium.

d) Optional Covers - Riders such as critical illness cover, accident cover, hospital cash, room-rent waiver etc. increase the premium.

Medical Insurance Tax Benefit

One major advantage of buying medical insurance is the tax benefit available under Section 80D of the Income Tax Act. You can claim tax deductions on the premium you pay for yourself, spouse, children, and parents. Individuals under 60 years of age are eligible for a tax deduction of up to ₹25,000, while senior citizens are eligible for a higher deduction of up to Rs. 50,000.

This benefit not only reduces taxable income but also encourages better financial planning.

Medical Insurance Plans

There are many medical insurance plans available in India for different medical and financial needs. Choosing the right plan depends on age, family size, lifestyle, and required coverage. Most insurers offer a wide range of plans from basic hospitalization cover to comprehensive policies with maternity benefits, critical illness cover, OPD care, and more. When looking for the best in India, you should consider:

a) High claim settlement ratio

b) Wide hospital network

c) Affordable premium

d) Flexible sum insured

e) Good customer service

Comparing different medical insurance plans helps you get maximum value for money.

What does Medical Insurance Basic Features Include?

A medical insurance plan generally includes:

a) In-Patient Hospitalization - Covers hospitalization expenses for more than 24 hours.

b) Pre & Post Hospitalization - That covers medical expenses incurred before hospitalization and after discharge for a defined period.

c) Daycare Procedures - Covers treatments like cataract, sinus treatment, and minor surgeries.

d) Ambulance Expenses - Covers road or air ambulance costs.

e) Domiciliary Treatment - Covers treatments at home when hospital admission isn’t possible.

f) Organ Donor Expenses - Covers organ donor hospitalization and surgery costs.

g) AYUSH Treatments - Covers Ayurveda, Homeopathy, Unani, Siddha, Yoga, and Naturopathy.

h) Annual Health Check-ups - Helps in early detection of health issues.

Exclusions in Medical Insurance

Medical insurance commonly exclude as follows:

a) Cosmetic surgeries unless medically necessary.

b) Routine dental, vision, or hearing treatment.

c) Lifestyle related diseases caused by smoking or substance abuse.

d) Self-inflicted injuries or suicide attempts.

e) Pregnancy related expenses unless covered under maternity benefit.

f) Diagnostic tests without diagnosis or hospitalization.

g) Drink and Drive.

How to File a Medical Insurance Claim?

1. Cashless claim process - When you are about to take your cashless claim then you have to submit below given documents.

a) Visit a network hospital

b) Show your policy card or number

c) Fill pre-authorization form

d) Hospital sends it to insurer

e) Once approved, treatment begins

f) Insurer settles the bill directly

2. Reimbursement claim process - In this process if you went to non-network hospital then you have to pay expenses from your side and then you have to submit the documents to your insurer. Documents list is as follows:

a) Pay the hospital bill at the time of discharge.

b) Collect the all original documents like bills, doctor consultation, payment receipts.

c) Fill the duly filled claim form and signed it.

d) Insurer verifies the documents.

e) Submit your kyc documents and cancel cheque.

f) After completed all documents, within 3 to 4 days you will received the claim amount in your bank.

Waiting Period in Medical Insurance

Waiting period in medical insurance refers to the time during which certain benefits of your insurance policy are not active. You can only claim for specific treatments or conditions once this time has passed. Every policy has different waiting timelines depending on the coverage. Here are some types:

1. Initial Waiting Period - The initial waiting period is the time during which you cannot raise a claim for any illness after buying your medical insurance policy. For the first 30 days, only accidental hospitalization is covered. Any seasonable disease like fever, dengue, malaria, etc. claim is accepted only after this period is completed.

2. Specific Waiting Period - The specific disease waiting period applies to specific disease such as hernia, piles, cataract, joint replacement, and similar conditions. These illnesses are covered only after completing the waiting period, which usually ranges from 1 to 2 years, depending on the medical insurance plans.

3. Pre Existing Disease Waiting Period - A pre-existing disease waiting period applies to any medical condition you already had before buying the policy, such as diabetes, hypertension, thyroid issues, asthma, etc. These conditions are covered only after completing 2 to 4 years of continuous policy coverage.

4. Maternity Waiting Period – The maternity waiting period applies if your medical insurance policy includes maternity benefits. Expenses related to pregnancy, delivery, and newborn care are covered only after completing the waiting period, which may vary from 9 months to 4 years, depending on the plan that you have opt.

Documents Required for Claim

When you file a claim under your medical insurance plans, the insurer verifies your treatment details and hospital records to process the request. Medical insurance policy ensures that you receive cashless or reimbursement claims without any kind of delays, by provided all required details correctly. Whether it’s a planned treatment or an emergency, proper documentation helps in faster claim settlement. In this insurance you can claim in types like in cashless or reimbursement claim so in future if you need to take any claim here are the documents list that you need.

1. Cashless Claim - For opting cashless claim you have to arrange following documents:

a) Policy Copy

b) Valid ID proof (Aadhar and Pan)

c) Doctor Advice

d) Pre-authorization form (Rest process will do by hospital TPA)

2. Reimbursement - For reimbursement claim you have to arrange these following documents:

a) Original bills

b) Payment receipts

c) Discharge summary

d) Consultation papers

e) Medicine bills

f) Diagnostic reports

g) Filled claim form

e) Cancelled Cheque

5.0

Need advice from experts?

Too many plans, too much confusion? We'll simplify everything for you, completely FREE. 100% honest, 100% spam-free.